Asia stocks climb tracking Wall St rally; Nikkei hits record high, China GDP beats

Introduction & Market Context

TEXT S.A. presented its Q4 2025/26 key performance indicators on April 7, 2026, revealing a strategic transformation underway at the global SaaS customer service platform provider. While monthly recurring revenue declined modestly, the company demonstrated significant progress in shifting its customer base toward higher-value clients and multi-product adoption, supported by AI capabilities that substantially outperform industry benchmarks.

The presentation highlighted both near-term revenue challenges and longer-term strategic positioning, as the company prepares to end price grandfathering and rebrand its product suite under the unified "Text" brand in fiscal year 2026/27.

Quarterly Performance Highlights

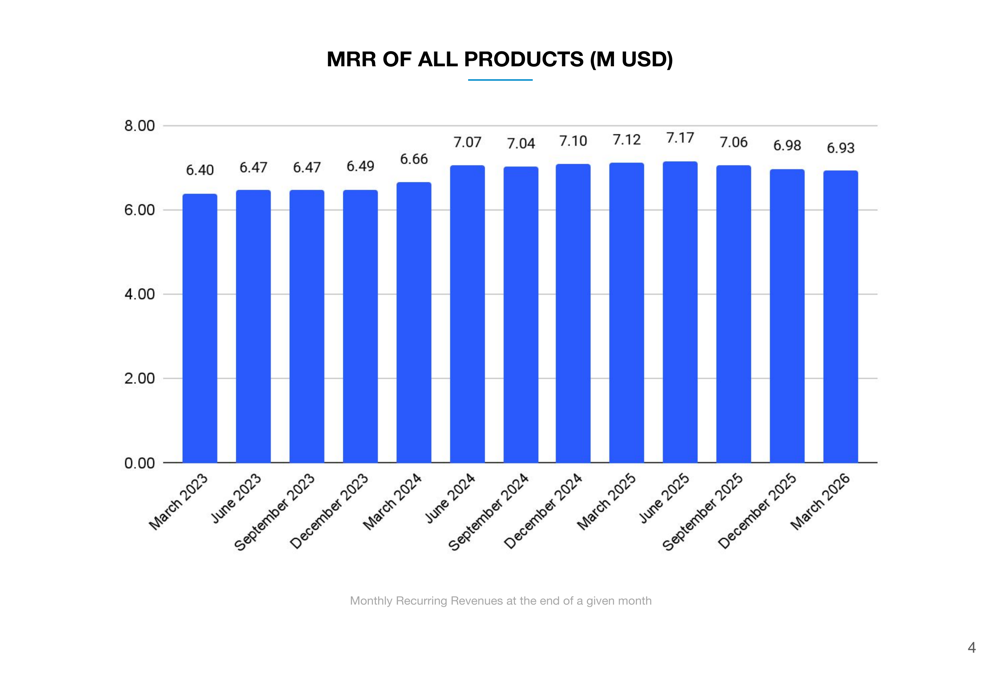

TEXT S.A.’s Q4 2025/26 results showed mixed performance across key metrics. Monthly recurring revenue fell 0.7% quarter-over-quarter to $6.93 million as of March 2026, continuing a gradual decline from a peak of $7.17 million in June 2025. The following chart illustrates the MRR trajectory over the past three years:

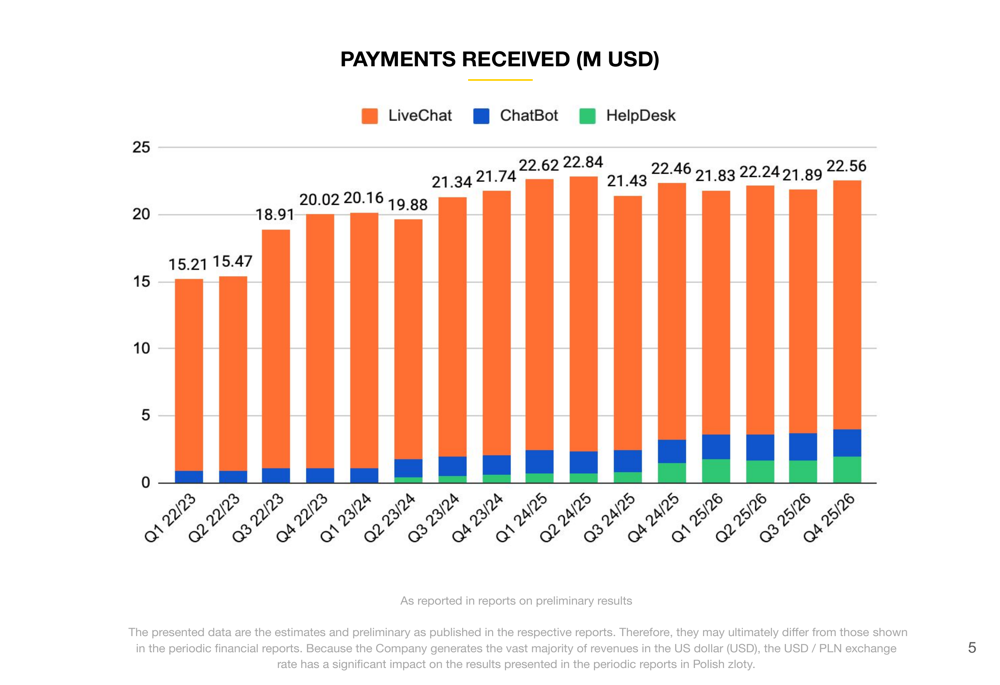

Despite the MRR pressure, payments received demonstrated resilience, increasing 3.1% quarter-over-quarter to $22.56 million in Q4. The company’s quarterly payment trends across its product portfolio show relative stability in the $21-23 million range:

API usage exceeded $250,000 during the quarter, representing an emerging revenue stream for the company. However, the presentation noted that payment data represents preliminary estimates subject to revision and USD/PLN exchange rate impacts.

Strategic Shift Toward Premium Customers

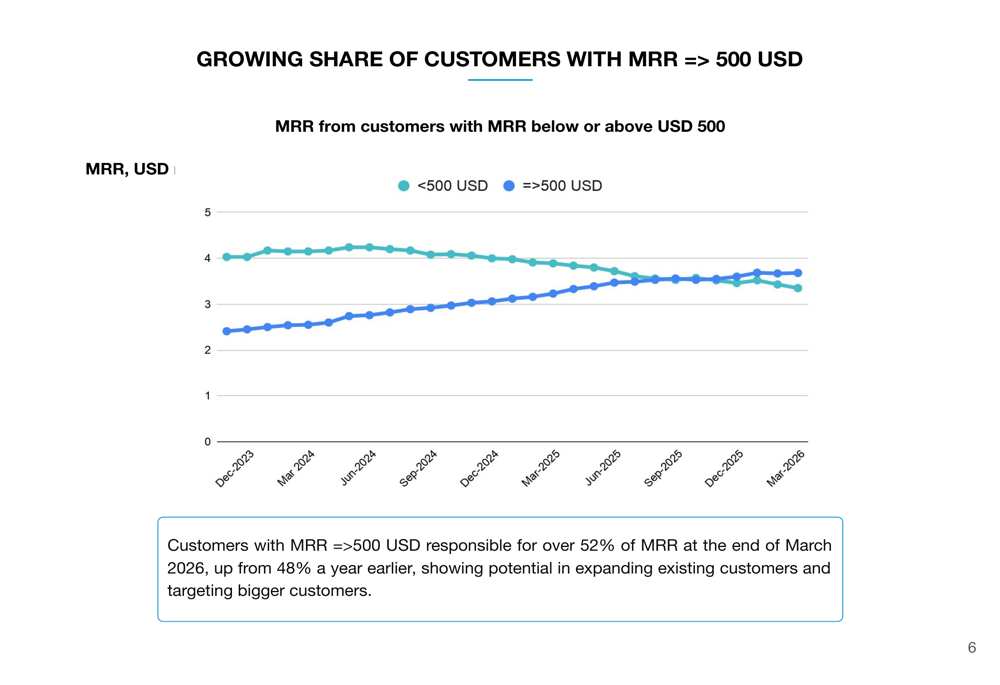

The most significant development in Q4 was TEXT S.A.’s continued success in cultivating a higher-value customer base. Customers with monthly recurring revenue of $500 or more now account for over 52% of total MRR as of March 2026, up from 48% a year earlier—a four percentage point increase that reflects the company’s focus on enterprise and mid-market clients. This strategic customer segmentation is illustrated in the following chart:

This shift toward premium customers represents a deliberate strategy to improve unit economics and customer lifetime value, even as it may contribute to near-term MRR volatility from smaller account churn.

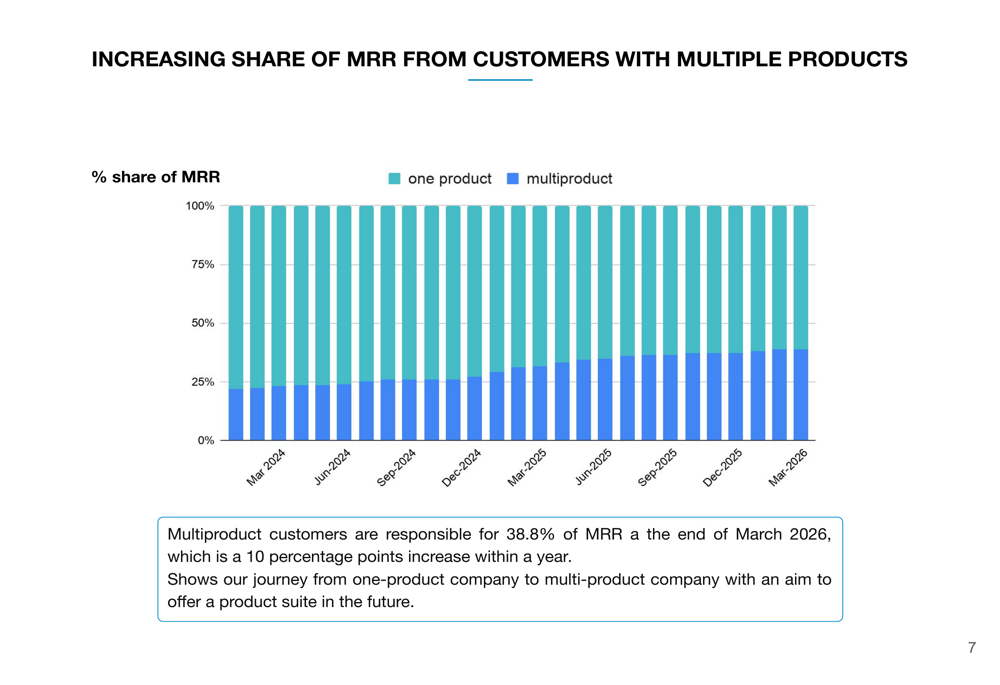

Complementing this premium customer focus, TEXT S.A. achieved substantial progress in cross-selling multiple products to its customer base. Multi-product customers now generate 38.8% of MRR, marking a 10 percentage point increase year-over-year. The company characterized this as evidence of its evolution "from a one-product to a multi-product company with an aim to offer a product suite in the future."

Product Innovation and AI Differentiation

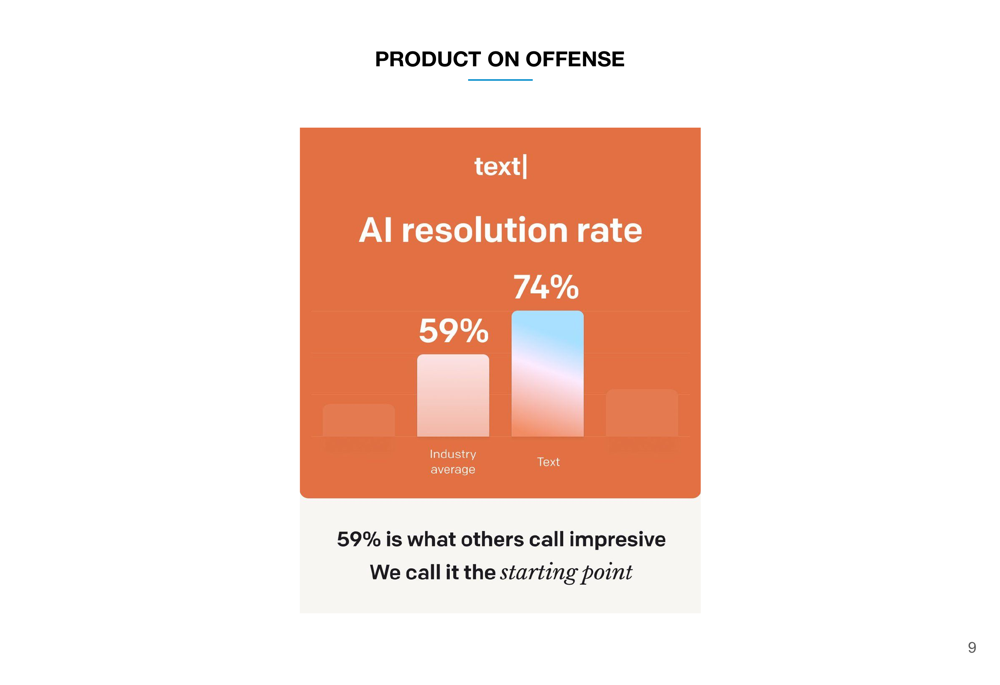

TEXT S.A. positioned its AI capabilities as a key competitive differentiator, claiming a 74% AI resolution rate compared to an industry average of 59%. The company’s tagline—"59% is what others call impressive. We call it the starting point"—underscores its ambition to lead in AI-powered customer service automation:

The company introduced major updates to its AI Agents during the quarter, including custom skills that convert intents into actions and the ability to deploy multiple AI agents within a single workplace. These enhancements aim to increase automation rates and reduce human agent workload for customers.

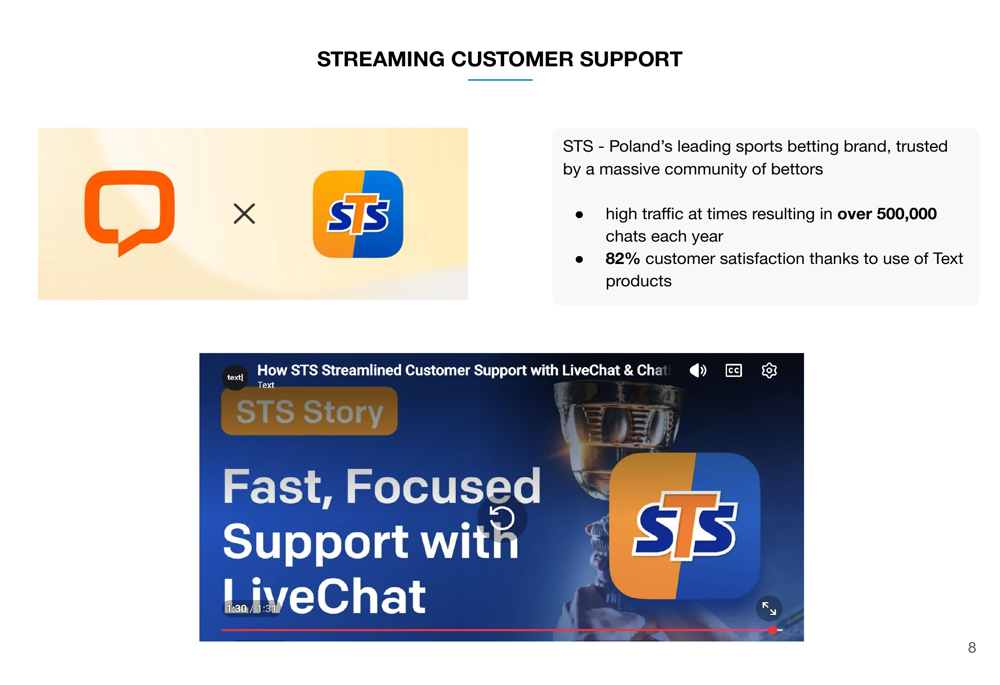

TEXT S.A. showcased STS, Poland’s leading sports betting brand, as a case study for its streaming customer support capabilities. STS processes over 500,000 chats annually using TEXT products and achieves an 82% customer satisfaction rate:

Market Expansion and Partnerships

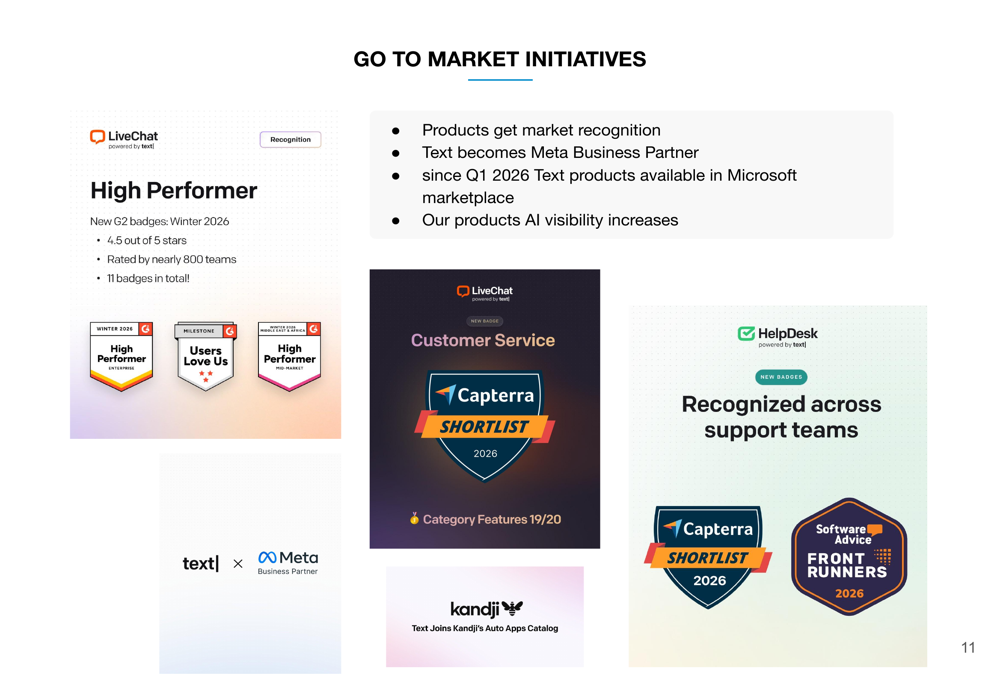

The company announced several go-to-market achievements that expand its distribution and market visibility. TEXT S.A. became a Meta Business Partner and made its products available in the Microsoft marketplace beginning in Q1 2026. The company also highlighted various industry recognitions and awards:

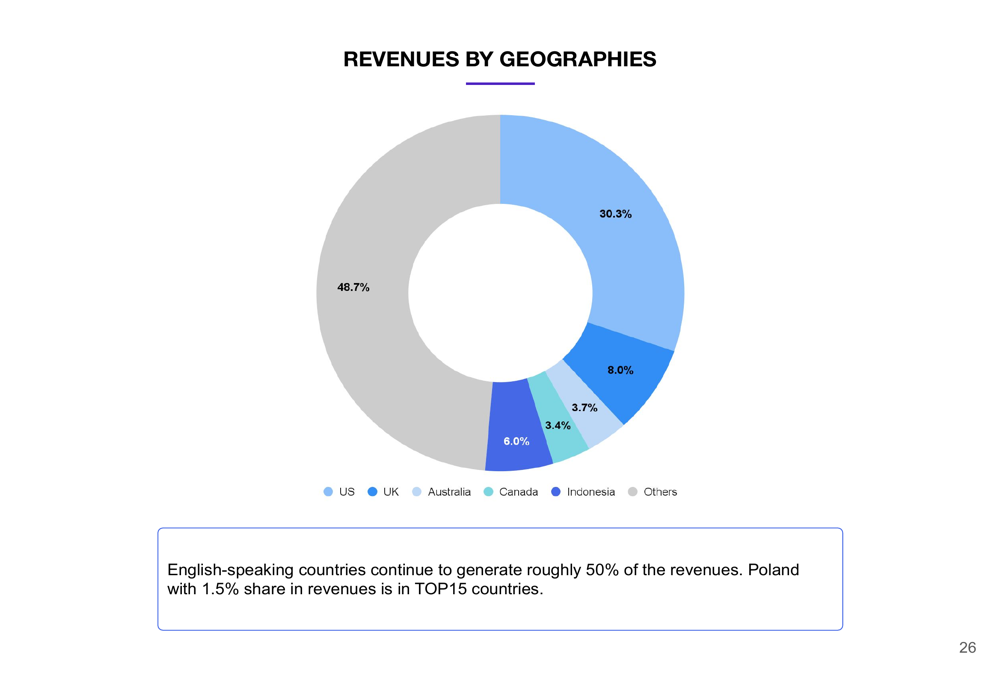

Geographically, TEXT S.A. maintains a diversified revenue base with the United States representing 30.3% of revenues, followed by a broad "Other" category at 48.7%, the United Kingdom at 8.0%, Australia at 6.0%, Indonesia at 3.7%, and Canada at 3.4%:

Financial Performance Details

The company’s financial results for the first nine months of fiscal 2025/26 (Q1-Q3) showed revenue and profitability pressure. Net sales declined 6.0% to PLN 249.2 million compared to the same period in the prior year, while EBIT fell 29.6% to PLN 96.2 million and net profit decreased 32.0% to PLN 88.1 million.

EBITDA for Q1-Q3 2025/26 totaled PLN 115.7 million, down 24.0% year-over-year, though the company noted that Q3 alone generated an EBITDA margin of 45.8%. Future revenues—a metric representing deferred revenue and contracted future payments—stood at PLN 66.1 million in Q3 2025/26, down from PLN 74.3 million in Q2 2024/25.

The revenue decline affected all three product lines. LiveChat, the company’s flagship product, saw revenues decrease while ChatBot and HelpDesk also experienced year-over-year declines. LiveChat continues to dominate the revenue mix, though the company is working to diversify through its other offerings.

Forward-Looking Statements

TEXT S.A. outlined several key initiatives for fiscal year 2026/27 that management expects will drive improved performance:

The end of price grandfathering will bring legacy customers onto current pricing structures, potentially improving average revenue per customer while risking some churn among price-sensitive accounts. The company is pursuing SOC-2 Type 2 certification to meet enterprise security requirements and unlock larger deal opportunities.

Most significantly, the company plans to officially roll out the unified "Text" brand to market, consolidating its product portfolio under a single identity. The presentation concluded by noting that the solution currently operating under the working name "Text App" would become "Text" imminently, with a "phased and scalable campaign" planned to support the rebranding.

The company highlighted notable contract renewals and upsells during Q4, along with new client acquisitions across virtually all industries, though specific customer names and deal sizes were not disclosed.

TEXT S.A. continues to operate as a dividend-paying company led by its co-founders, with a shareholder structure that includes a 41.3% agreement of shareholders, 43.1% free float, and stakes held by Allianz Polska (6.2%) and NN Polish pension funds (9.4%). The company employs over 250 team members globally and maintains its positioning as a B2B SaaS business with a subscription revenue model.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.